Long Memory Analysis

Methods used in the analysis of long range dependence (long memory) are constantly under study. Since Hurst and his R/S analysis new methods have been developed. A lot of these methods are just helpful tools through which we "see" the world in a different way. Some of them have not been fully understood yet, but have proven usefull for analysis of long memory.

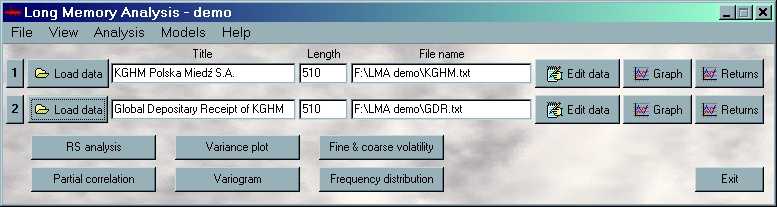

Long Memory Analysis (LMA) v. 2.0 is a program developed recently for analysis of long range dependence in financial time series. It contains such methods of analysis as: R/S statistic, V statistic, partial (lagged) correlation, variance plot, variogram, and fine&coarse volatility. Moreover, it allows estimation of parameters and generation of trajectories of a few heteroscedastic models (ARCH, GARCH, TARCH and HARCH).

LMA v. 2.0 (full version) - ok. 0,8 Mb (exe only)

The demo version allows you to analyse long memory of nine included data sets, as well as, analyse and generate financial time series no longer than 500 values (which roughly corresponds to two business years). The full version of the program does not have these limitations. In case of questions please contact the authors:

Rafał Weron: rweron@im.pwr.wroc.pl, Andrzej Zacharewicz: zachar@techland.com.pl